VANCOUVER — Canadian exports of liquified natural gas (LNG) face an increasingly uncertain global market as the US and Qatar bring cheaper large-scale production online, and many countries decide to leapfrog directly from coal to low-cost domestic renewable energy.

“Global LNG markets have been upended by the conflict in the Middle East,” said Ian Sanderson, senior analyst at the Pembina Institute, in his new report The LNG Gamble – Separating Hype from Reality. “Prior to the conflict, the largest build out of supply in history was already underway, raising concerns about a looming supply glut and falling prices.”

Instead, the closure of the Strait of Hormuz and damage to LNG infrastructure in the region has flipped the market into shortage and an 80 per cent price spike. While some argue this creates an opportunity for Canadian LNG to fill the supply gap, the severity of the disruption is more likely to permanently reduce the demand for LNG altogether as importing nations turn toward cheap and secure domestically produced renewable energy. For example, Vietnam recently abandoned plans for a new 4,800-MW LNG power plant — nearly four times the capacity of B.C.’s Site C hydroelectric project — in favour of a renewable energy and storage system.

“The biggest risk now facing LNG sellers is that importing countries will realize there are much more secure and much cheaper options available,” Sanderson said.

The LNG Gamble examines the LNG demand outlook in China, Japan, South Korea, and India. In all cases, LNG demand declined in 2025. Potential for future growth is highly uncertain as governments pivot towards options with less price risk exposure, including renewable and nuclear generation. The role LNG might play in their future planning will be highly price-sensitive, which favours producers in the US and Qatar.

“Canadian LNG investments now face a dual threat: demand destruction in the near term from high prices, followed by a likely glut of supply later this decade,” Sanderson said. “Together, these forces increase the likelihood of stranded assets, elevate risks to public finances, and undermine Canada’s climate commitments.”

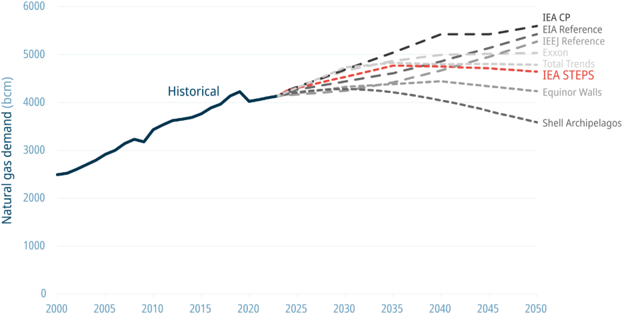

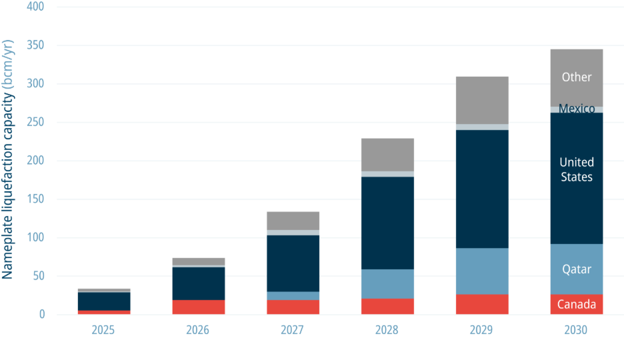

Most industry modelling (above) published before the start of the Iran war indicated global gas demand would plateau or decline around 2035. Sharp changes in energy policy in importing countries will likely bend all these trajectories downward. Meanwhile, planned new LNG projects will lead to a large oversupply (below).

Coal-to-gas switching is often cited as a way for LNG to reduce global emissions. However, Sanderson notes that IEA modelling indicates significant switching would require LNG prices to stay well below US $5 per million British thermal units, which is less than half of the pre-war global price average and only marginally higher than average production costs for Canadian terminals.

“This creates a structural problem for Canadian LNG,” said Sanderson. “The price necessary to displace coal is a price that would severely damage the business case for new Canadian projects. Conversely, as prices for renewable energy have plummeted over the last decade, buyers have cheaper, cleaner and local options to replace coal.”

“Governments should not step-in with public dollars to de-risk further LNG projects,” Sanderson said. “LNG Canada Phase 1, Cedar LNG, and Coastal Gas Link received $1.6 billion in public financing and direct support. LNG Canada Phase 2 and Ksi Lisims are on the major projects list and have received all the necessary approvals for a final investment decision to be made. Private proponents, not Canadian taxpayers, should be left to take on the risks of investing in LNG markets.”

[30]

Contact

Benjamin Alldritt

Senior Communications Lead, Oil & Gas

587-328-1955

Background

Report: Power Struggle