Last November, when Alberta and Ottawa signed their memorandum of understanding on climate and energy, the airwaves, podcast feeds and column inches were suddenly awash with commentators discussing this specific line from the agreement:

“The TIER system will ramp up to a minimum effective credit price of $130/tonne.”

To those of us who carefully track TIER and the efficacy of that regulation, it was music to our ears. Sorting out issues with the effective price – and thereby fixing TIER’s broken credit market – is one of the most critically important things that must happen to speed up the deployment of potentially billions of dollars of low-carbon investment in Alberta. The fact that both Premier Smith and Prime Minister Carney recognized the importance of instituting a minimum effective price deserves recognition, praise and ongoing support from anyone who cares about the future of Alberta’s and Canada’s economy over the next several decades.

But... it’s also a little difficult to praise something that is, ultimately, very hard to understand.

I mean – what even is the “effective credit price”, anyway?

TIER is the Technology, Innovation and Emissions Reduction regulation, the full name of Alberta’s industrial carbon pricing system. It’s been in place in one form or another since 2007, and for the majority of that time enjoyed the vocal support of industry, including oilsands executives, who praised how it incentivized investment in clean technologies but did so in a fair, predictable manner that they could work into their business planning.

But TIER is also, necessarily, extremely complex. That’s unsurprising, given it simultaneously encourages major investments in emissions reduction projects, while minimizing the costs to industry to as little as a few cents – the cost of a timbit – per barrel of oil. And that complexity has led to widespread confusion in the months since the MOU was published.

For example, the headline price of carbon in TIER is already scheduled to rise to $170 by 2030 – a price widely agreed to be necessary for very expensive technologies like carbon capture and storage to become viable.

So, when the MOU stated a $130 price, some pundits thought that Alberta had essentially negotiated a $40 discount (and a key climate policy concession) from Ottawa.

Others mused on whether $130 was affordable. Did that mean the companies would have to pay tens of dollars of carbon tax for every barrel of oil they produced?

Unfortunately, both these takes (and many others that have been floating around since late last year) misunderstand a fundamental aspect of large emitter trading systems, like TIER: the headline price is different (although related) to the effective price. This underscores one of the major risks of taking an extremely complicated regulation like TIER and making it part of such a public negotiation like the MOU - it leaves lots of room for misunderstanding, and even gamesmanship. When confusion abounds, it’s not easy for Canadians to tell whether they’re being presented with a solution that’s broadly good, or broadly bad.

That’s why we’ve been saying that the one key metric we’ll be using to judge the deal that’s presented on April 1 is if the agreed-to $130 per tonne minimum effective price will be reached by 2030 at the latest. (More on our MOU-must-haves here!)

But if you don’t happen to have an advanced degree in climate policy or economics and therefore you don’t instinctively know the difference between the effective price, the headline price, or why either of those prices matter to how TIER works to reduce emissions, then the reasons behind our $130-by-2030 ask are almost certainly still a mystery.

So, brace yourself, reader, for industrial carbon pricing 101...

But first

A disclaimer for all the true TIER fans out there: this article is going to include some areas of simplification. The priority is to explain the broad strokes of the system and the different prices within it – but that means in some places I’ll cut corners with the level of detail I get into.

A quick re-cap on how TIER works

For almost 20 years, industrial carbon pricing systems in Alberta have been reducing emissions from heavy industry. They do this by correcting a market failure: making it no longer free for companies to pollute.

Because, when there’s a real financial cost associated with polluting, there’s a business reason to stop doing it.

In TIER, this works like this:

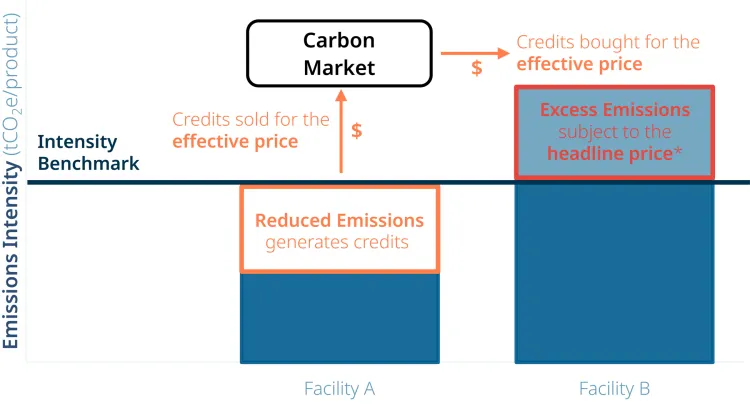

- Every regulated facility (say, an oilsands mine) is given a “benchmark” that is the exact level of pollution they are currently “allowed” to put into the atmosphere for free. This is calculated a few different ways: either by looking at a facility’s historical performance, or by looking at all facilities of a similar type (so, all oilsands mines) and assessing what the average level of emissions already is for the top 10% of performers, to then determine a reasonable place for the benchmark to be set.

- If a facility’s emissions are above the relevant benchmark, every excess tonne is, in theory, subject to the headline carbon price. Right now, the headline price is $95 per tonne.

- In reality, companies don’t usually end up paying the headline price. Instead, they have the option to purchase credits to cover their excess emissions.

- Credits are generated by other facilities who outperformed – meaning those whose emissions are below their benchmark.

- The price those carbon credits are sold for (from the high-performing oilsands mine, to the other oilsands mine) is the effective price.

Fig 1. The principles of TIER's emissions benchmarks and carbon market. *Note, most facilities do not actually pay the headline price, but meet their emissions obligations by purchasing credits instead.

Overall, this complicated system has two effects: it rewards facilities that reduce their emissions early, and it also incentivizes companies to build projects and technologies that will reduce their emissions in future – because they know they will be able to defray the cost of that investment with the guarantee of credits that they will be able to sell.

The system is then supposed to be tightened over time

The next key part is ensuring that emissions don’t just stay at an appropriate level, but decrease further over time. This is supposed to be done in two ways:

- The benchmarks get lower every year.

- The headline price rises each year.

Both of these things are meant to be scheduled ahead of time, so companies know what to expect. This means they can calculate how much it would cost them to pay the headline price in, say, five years’ time – based on the price for that year, as well as how many tonnes over that year’s benchmark they’ll likely be emitting.

And this is where one of the most important principles of industrial carbon pricing comes in:

At some point, the headline price needs to be high enough, and the benchmarks need to be low enough, that a company would be financially better off investing in emissions reduction technologies now than by paying the headline price in future.

…but…

This whole principle falls apart if companies can meet their emissions obligations by buying very cheap carbon credits.

And that’s why the MOU commitment to a minimum effective price is so important. The effective price is what companies pay for compliance overall, including the price of credits in the marketplace, and is generally lower than the headline price, but shouldn’t be drastically lower.

Unlike the headline price, the effective price isn’t explicitly set by government. But government actions can still affect it

Alberta’s carbon credit market is just like any other market: supply-and-demand is king. When there’s lots of credits available for purchase, but demand for those credits is low, the effective price goes down. When there are fewer credits available to purchase than facilities wanting to purchase them, the effective price goes up.

However, while the government doesn’t explicitly get involved in setting prices, it can still have a significant impact on them, depending on how it chooses to administer the TIER system. Indeed, in the last twelve months, Alberta has made some key changes to TIER that have undermined credit prices:

- Failing to tighten up facility benchmarks

When benchmarks are set too high, it becomes easy and relatively cheap for companies to invest in low-hanging-fruit projects that reduce their emissions below them. An example would be a company switching out all its lightbulbs for high-efficiency bulbs – a relatively cheap endeavour. When companies can generate credits this easily, it drives up credit supply and drives down the effective price. A good way to think about this is companies being over-rewarded for their behaviour. - Freezing the headline price

As opposed to flooding the market with credits, this reduces demand for credits (which, nevertheless, has the same devaluing impact on the effective price). This is because, if the headline price isn’t rising quickly enough (or at all), companies may make a judgement that further investment in decarbonization isn’t necessary, since the price will not be increasing over time. Instead, they’ll choose to either just pay the headline price or purchase credits that are cheaper than investing in emissions reductions. - Introducing a new option within TIER that credits investment, rather than emissions reductions

Late last year, after the MOU was signed, Alberta pushed through previously announced regulatory changes that opened up a new option within TIER, called a direct investment mechanism. In essence, this allows companies to generate credits at the point of investment in a supposedly emissions-reducing project, and also at a later date when (or if) that project results in actual emissions reductions.

The problem with this is twofold. First, it introduces the concept of double-counting; two credits are being given instead of one, exacerbating oversupply in the credit market. Second, there is little to stop companies making relatively inexpensive investments that, ultimately, may have no impact on their emissions. An example would be a company investing in an engineering study of a CCS project. Eventually that study might lead to a project that, once built and operating, might result in emissions reductions – but it’s a lot of steps from point A to point Z, and no guarantees that promised emissions reductions will be delivered in full and on time. Awarding credits based on investments rather than emissions reductions fundamentally undermines the point of the system – which is for companies to invest now in order to reduce emissions and therefore avoid paying (either the headline price or the effective price) at a later date.

Because of these combined factors, for much of the last year, TIER’s credit market has been in a mess. Credit oversupply has reached critically bad levels, and for periods of months, the effective price was as low as $20 per tonne. When credits are that cheap, the whole system stops functioning properly, clean investment comes to a standstill and emissions reductions plateau.

The magic of a guaranteed $130 minimum effective price by 2030

As this whistlestop tour of TIER has shown, the whole system is reliant on investors having a certain level of confidence that the initial principle – that industrial carbon pricing will make it no longer free to pollute – will be upheld over time. In other words, they need to be reasonably sure that if they spend money today on a project that will only start to reduce their emissions three, five, or ten years from now, the credits they will generate later will still hold a reasonable value.

And so, this is why the MOU commitment – signed by both Alberta and the federal government - to reaching a $130 minimum effective price was so very heartening. What we now need to see is that the $130 minimum effective price is reached by 2030 at the latest – as it’s the thing that will kickstart investment in emissions reduction projects over the next few months and years. The sooner it’s scheduled, the sooner companies have can move ahead with potentially billions of dollars of job-creating investment across multiple heavy industrial sectors - investment that Alberta has been missing out on while the TIER market has been bottoming out for the last couple of years.

What’s more, as shown by the latest Canadian Climate Institute analysis, ramping up to $130 will, on average, cost oil producers about 50 cents on the barrel. Far from being a system that undermines the competitiveness of our oil exports, TIER is a system that catalyzes low-carbon investment from oilsands companies, while also bolstering the business case for other emerging low-carbon industries.

Because we aren’t only talking about finally moving ahead with CCS in the oilsands (the Pathways project), but also investments in low-carbon cement, hydrogen, and petrochemical facilities that will create products that the world is increasingly demanding; renewables development to improve Alberta’s capacity of low-cost electricity; and other areas of the low-carbon industrial economy that have yet to be explored in the province. In short, TIER has a huge role to play in futureproofing Alberta’s economy, and urgently achieving a guaranteed minimum effective price is step one in restoring investor confidence and forging ahead.