Over the past two decades, oil and gas pipelines have emerged as potent political symbols. In 2019, Jason Kenney ran a successful provincial election campaign in Alberta with the slogan “Jobs – Economy – Pipelines.” In 2025, oilsands producers bought billboards across Alberta that read “It’s not just a pipeline, it’s a stronger economy.” At the same time, the protests and lawsuits surrounding Northern Gateway, Trans Mountain Expansion, Keystone XL, Dakota Access Pipeline, and Coastal Gaslink have turned pipelines into opponents’ shorthand for industry’s disregard for climate change and government’s disregard for Indigenous communities.

Over that period in the United States, Keystone XL was proposed then cancelled then approved then cancelled again and now will potentially be resurrected yet again, depending on the government of the day.

But underlying all this political symbolism is a simple reality: a pipeline is a business venture. Building or blocking a pipeline is an emotional issue for politicians and their supporters, but investors risk their capital only because they’re confident the project is going to pay back their investment and make enough profit to justify the risk. When the project costs tens of billions of dollars and must operate for decades into the future, that confidence demands a thorough and unemotional analysis of risks and benefits.

Of course, the math around a pipeline gets a lot easier if you can “de-risk” a project by gambling with someone else’s — the taxpayer’s — money.

The attack on Iran, which has damaged energy production infrastructure and intermittently closed the Strait of Hormuz, as well as the U.S. government’s military intervention in Venezuela, have prompted more voices to call for Canadians’ tax dollars to be put towards a new oil export pipeline from Alberta to B.C.’s Pacific coast. This is despite the Governments of Canada and Alberta proclaiming in their November 2025 memorandum of understanding that any new pipeline must be “private sector constructed and financed.”

Public financial support for industry can take many forms, and at times is warranted in the case of genuinely emerging, innovative sectors that may benefit from time-limited assistance to establish themselves or gain a competitive advantage. In fact significant provincial and federal taxpayer dollars went into the creation of AOSTRA and Syncrude to make the oilsands economically viable. Canada’s oil sector, is now well-established wildly profitable, and no longer fits the bill for continued taxpayer subsidies; oilsands firms brought in $178.3 billion in revenues in 2025, despite weak oil prices — and revenues are poised to jump this year as a result of the U.S. incursions. There are many different ways to earmark public funds for industrial growth; direct cash injections are the most obvious and cost the most, but also tax relief, preferential loans, tax credits, and suspending regulatory requirements are all types of financial support that lower the cost of doing business. Some of those measures are less costly to the Canadian public than others — a tax break represents lost potential revenue but doesn’t require additional funding from the government. But that’s potential revenue that could be earmarked for other uses, particularly in a time of significant budget deficits. As negotiations continue between Alberta and Ottawa on that memorandum, Prime Minister Mark Carney must keep his promise to Canadians that public dollars won’t be spent building a pipeline. Here’s why:

Investors remain skeptical

For many years, energy sector executives and Alberta provincial leaders protested that the Trudeau government’s environmental legislation prevented pipelines from being built. No one, they argued, would invest their time and money in a project which could spend a decade or more trying to satisfy the federal Impact Assessment Act — dubbed the “No More Pipelines Act” by then-Premier Jason Kenney — and then figure out how to increase production to fill it under a potential emissions cap, only to reach a coastline with a legislated ban on tanker traffic.

Those arguments cannot be made today. Carney has promised a two-year process to clear a path for “nation-building” projects and deputized a former pipeline executive to run his new Major Projects Office, headquartered in Calgary. He has committed to rolling back the tanker ban and the never-implemented emissions cap, in the service of getting one or more new export pipelines built. And if the Carney government should fall, there’s an even more pro-pipeline Loyal Opposition waiting in the wings.

With all this regulatory and political risk cleared away, you would expect oilsands producers and pipeline companies to rush forward with proposals or at least signal their intent to bring one forward . . . but they haven’t. Back in June of 2025, Alberta Premier Danielle Smith confidently predicted she would find a private sector proponent “within weeks.” But to date, the only proponent is Smith herself, who put up $14 million of Alberta taxpayers’ money to start developing a plan. Several pipeline companies agreed to join an advisory committee, but none of them have invested a dollar in this venture.

If regulatory risk isn’t keeping investors on the sidelines, then what is?

China’s energy transition is booming

Having the world’s largest economy on our doorstep has been a wild ride for the Canadian oil business. Exports to American refineries, calibrated for Canadian heavy crude, more than doubled from 2005 to 2025. But hyper-dependence on the United States has its pitfalls, including price discounts on Canadian oil. The Trans Mountain Expansion was built to expand Alberta’s access to overseas customers, and primarily the world’s second-largest economy — China.

China, however, is now working overtime to use less oil. In March, the Chinese government approved a new Five-Year Plan, and the framework text includes the explicit goal of “peaking petroleum demand.” This isn’t just aspirational talk. Chinese drivers bought 37,000 new electric vehicles every single day in 2025. Beijing’s motives are economic and geopolitical. The cheapest way for 1.4 billion people to get around is in electric vehicles charged by low-cost renewable generation. Ramping up domestic renewable generation also reduces China’s exposure to global risks such as the closure of oil and gas exports from the Persian Gulf, or unpredictable US trade policy. Analysis from Chatham House suggests that China has concluded that “no great power can afford to be at the mercy of another’s supply chain.”

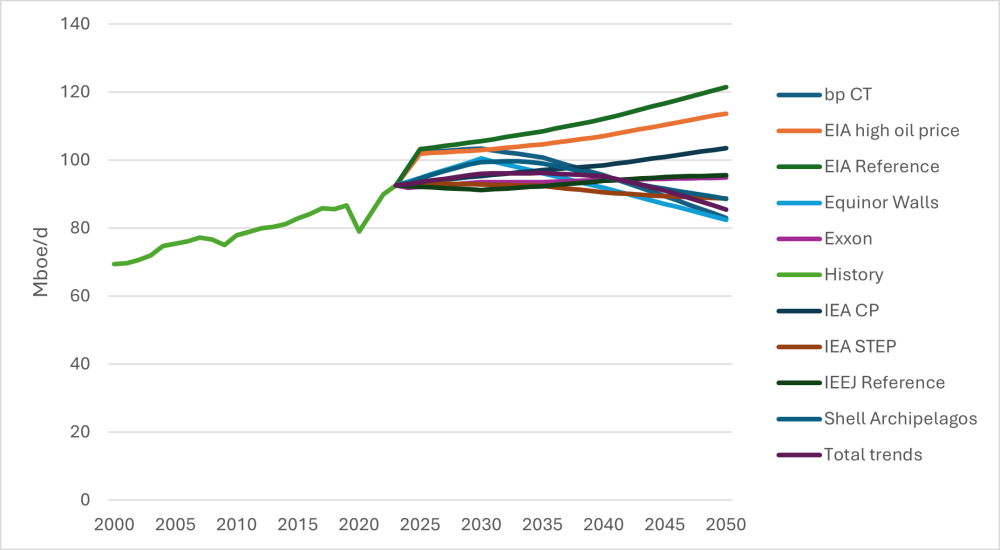

Analysis from BP, Shell, Equinor, the International Energy Agency and others all reflect this shift. In their Current Trajectory model, BP maps out an energy future where the world continues with existing policies, and “in marked contrast to the past decade during which China accounted for around half of all global oil demand growth, China’s oil consumption is slightly lower by 2035.” This model suggests a global demand peak of around 103.4 million barrels per day in 2030, followed by a steady decline to around 85 million barrels per day (i.e., less than current demand) by 2050.

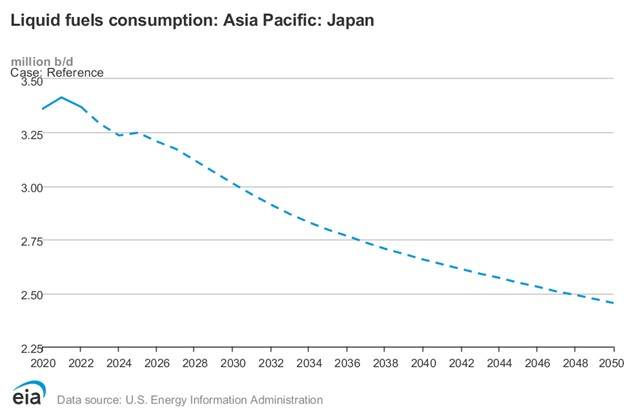

China is not the only Asian economy highlighted as a possible destination for Canadian crude where oil demand shows signs of long-term structural decline. Japan’s oil consumption is projected to steadily decline in the United States Energy Information Administration’s Reference Case.

Shell published three scenarios with varying emphasis on climate change response, energy security concerns, and rising energy demand from escalating AI and quantum computing use. All scenarios foresee a demand peak in the coming decade followed by permanent declines of varying steepness.

A new Canadian pipeline would come into service just as global oil demand enters an era of irreversibly softening demand and price. This is a sobering thought for an investment of around $50 billion for a new pipeline, plus considerably more investment in new oilsands production facilities to fill it.

Figure 1: Across most scenarios from a variety of private sector and energy organizations, oil demand flattens and begins to decline

War in the Middle East will drive more oil importers to choose a new path

Another argument offered in favour of a new pipeline is that war in the Middle East will increase demand for politically stable and physically secure sources of oil. That may be true in the short term but it’s actually an argument against public subsidy; if world events are making Canadian oil more attractive to customers, then that should reduce the need to prop up its business case with taxpayers’ money.

The longer-term effects of conflict in oil and gas producing regions, however, should be more troubling than encouraging for pipeline supporters.

Following Russia’s invasion of Ukraine in 2022, European nations scrambled to find other sources of natural gas. But four years later, Europe is doubling down on low-cost renewables as a permanent and secure energy source. With freedom to navigate the Strait of Hormuz uncertain, volatile oil prices, and the likelihood of regional unrest for an indefinite period to come, oil importing nations, and their drivers, will be making similar calculations.

Canada may be a safe and stable place to send tankers, but it’s still part of a global oil market. Prices for Western Canadian Select have spiked to as much as twice their pre-war level in recent weeks. An electrified road transport fleet charged with domestic low-cost renewable energy is a compelling way to protect a country’s economy, and the driving public, from volatile fossil fuel prices.

These pressures have the potential to accelerate the China-led decline in global oil demand for transportation use. High prices mean a windfall for oil companies and oil producers like Canada in the short-term, but they also set the stage for demand destruction in the longer term, which is another significant risk factor for capital investment in oil infrastructure.

There are lower-risk options available

In the days following their seizure of Venezuela’s president, American officials suggested that a rehabilitation of that country’s decrepit oil industry was one of their goals. The possibility of increased Venezuelan heavy crude production, and its potential to displace Albertan heavy crude at American complex refineries, led some Alberta industry leaders to argue that a new pipeline was needed simply to protect existing business, let alone expand it.

Major investment in Venezuelan production is by no means certain, and its impact will be many years away if it does come to pass. But if the solution to increased competition in the Americas is to sell more oil to China, given the declining Chinese demand that the oil industry already expects, then this simply increases the risk of a new pipeline becoming a very expensive stranded asset.

Canadian taxpayers already own the Trans Mountain pipeline (TMX), which the Trudeau government bought from Kinder Morgan in 2018. It’s still not being used to its full capacity, and some further work could increase its capacity by roughly 300,00 barrels per day, or about a third of a new pipeline. The B.C. government has also expressed some grudging support for this option, which would include upgrading pumping equipment along the pipeline and dredging Port Metro Vancouver to allow supertankers to depart with a full load.

This additional export capacity can be found without disturbing a new path across northern B.C., lifting tanker restrictions, or creating conflict with rights-holding First Nations on the coast. This option gives oilsands producers some runway to increase production in a shorter timeframe without the risk of stranding tens of billions of dollars in a whole new pipeline.

Politicians are drawn towards wholly new projects that they can claim some credit for. But sometimes, a pipeline has more value to elected officials as a political symbol than it does to investors as an economic asset. Investors should decide whether a TMX upgrade is sufficient to meet their needs without taking on undue risk.

A pipeline doesn’t bring Canadians together

In addition to economic, environmental and geopolitical pressures, the federal government must also be sensitive to matters of national unity. The possibility of two separatist referenda in Canada — in Quebec and Alberta — is quite real. A large-scale demonstration of federal support for Alberta’s pre-eminent industry would be an obvious move to help tamp down western alienation. But spending Canadian taxpayers’ money on an Alberta pipeline may actually deepen divisions across Canada.

Alberta remains by far the province with the highest carbon emissions, and the increased oil production needed to fill a new pipeline, even when coupled with the Pathways carbon capture project, will increase the climate-changing emissions from the oilsands even more. How can we reasonably ask families and businesses in every other part of Canada, including Quebec, to reduce their own emissions while also compelling them to subsidize rising emissions in Alberta?

Let investors decide if the risk is acceptable

Businesses will always be eager to accept a gift of public money, and politicians will always be tempted to help break ground on a megaproject. But it’s not the taxpayer’s job to finance a private company’s spin of the roulette wheel. If the risks of building a new pipeline are acceptable to a private sector proponent, then they should be free to gamble their own money and enjoy the profits if they’re proven right. But if the risks are too great for shareholders, then they’re too great for taxpayers. A pipeline is a business venture, and it should be able to stand on its own merits if it’s a wise one.