This is the year. 2015 is being widely proclaimed as the year the world’s governments get serious about climate change. Talks will be held in Paris in December and discussions are already underway about what needs to be done, what jurisdictions are willing to do and the impacts of action. One undeniable consequence will be stranded assets. This is particularly true in Alberta where oil production is on the higher end of the scale for both cost and carbon emissions.

So, what exactly are stranded assets? HSBC has released a new report that provides a concise definition. "Stranded assets are those that lose value or turn into liabilities before the end of their expected economic life. In the context of fossil fuels, this means those that will not be burned – they remain stranded in the ground."

This is becoming a hot topic. There has been a growing dialogue about the risk of stranded assets related to climate change and carbon regulation over the last few years. During 2014 in particular, it reached mainstream discussion with experts ranging from the World Bank Group president, Jim Yong Kim to former Bank of Canada governor, Mark Carney, issuing warnings about this risk.

The Pembina Institute has also been tracking this issue. Last November we helped organize a cross-Canada tour for James Leaton of Carbon Tracker — one of the leading voices in highlighting the financial risk of stranded assets. A Day of Learning organized with RBC, NEI and Suncor also helped raise the level of dialogue on this issue in Canada.

The HSBC report — Stranded assets: what next? — is particularly interesting because it moves beyond the original framing of the risk of stranded assets being the consequences of governments implementing policies that accelerate the transition to cleaner sources of energy — resulting in fossil fuel reserves going undeveloped. HSBC digs deeper and points to two additional sources of stranded assets risk – the current and future price of oil and the risk presented by innovation in the energy system.

Risk 1: Stranded by policy

This is where the stranded assets discussion started. A number of organizations have laid out their estimates for humanity’s carbon budget – the total amount of carbon pollution that can be emitted while still having a chance of limiting climate change to the 2C globally agreed upon goal. All of these carbon budgets require that a portion of known fossil fuel reserves remain in the ground.

For oil and natural gas the discussion is still in the future risk space, but we have seen this play out for coal. The coal industry in the U.S. has lost 76 percent of its value in five years and it’s looking more and more likely that a significant portion of U.S. coal reserves will remain in the ground.

Risk 2: Stranded by price

Beyond climate regulation, the report points to economic drivers that could strand fossil fuel assets. Since November of last year oil prices have fallen dramatically, bringing pricing related challenges back in to focus. We have seen a wave of capital expenditure reductions and lay offs across Alberta’s oilsands with the value of oil and gas companies globally dropping by over US$580 billion.

Beyond the current oil prices, there are many other factors that could impact the economics of production – higher taxes on earnings, removal of subsidies or increases in the cost of production to name a few.

Risk 3: Stranded by innovation

The third risk identified in the report is energy innovation – both from efficiency (which decreases overall demand for energy) and disruptive technologies (that change the energy mix and likely reduce demand for fossil fuels).

Efficiency drivers – Globally, GDP remains closely aligned with increasing energy consumption. The European Union has mandated energy efficiency targets and appears to be decoupling GDP growth from energy use. The authors of the report feel the EU example represents what can be achieved globally.

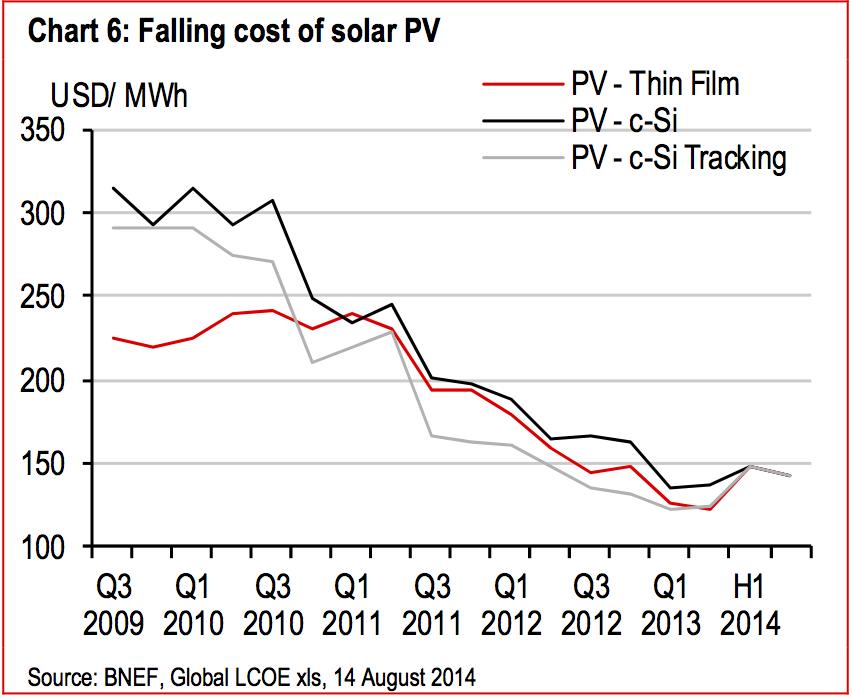

Technology drivers – Renewables, electricity storage, and enhanced oil recovery could drive future stranding. The rapid drop in renewable’s costs could trigger a purely economically driven decarbonisation of the power sector.

Electricity storage technologies have been rapidly entering the mainstream. If they continue to come down in price and improve in performance, they will enable both increased adoption of renewables and make more affordable electric vehicles a reality – both impacting demand and pricing for fossil fuels.

Electricity storage technologies have been rapidly entering the mainstream. If they continue to come down in price and improve in performance, they will enable both increased adoption of renewables and make more affordable electric vehicles a reality – both impacting demand and pricing for fossil fuels.

What should investors do?

The second half of the report presents a few options for how investors could manage fossil fuel investments. First would be identifying companies that have assets that are most at risk for stranding — producers of fossil fuels and companies along the value chain that are major emitters like coal reliant electricity generators. Second is deciding how to manage that risk — with some degree of divestment, or hold and engage being the two options.

What should Alberta do?

Throughout the last decade, the oilsands sector has grown in importance to Alberta and Canada. But given the world’s increasing focus on climate change negotiations, it may be time to ask where Canada’s oil and gas sector is going in the future.

High cost, high impact oils are particularly sensitive to the stranding risk. Given that oilsands disproportionately fall into that category, Canada and Alberta should take note of the material risk stranded fossil fuel assets pose to investors and their own coffers alike.

As Alberta looks to renew its climate change strategy, it’s essential to take stock of these economic and environmental trends and respond with an ambitious plan to reduce the province’s carbon footprint. To this end, British Columbia provides a good example of a successful approach in reducing carbon pollution while encouraging economic growth and innovation.

If Alberta wants to ensure its natural resources generate value – not liability – for generations to come, it must tackle the climate challenge head-on.