CALGARY — New research from the Pembina Institute finds that for the first time since the pandemic, companies are allocating capital to increase their production – but are still yet to make meaningful investments in projects to reduce emissions.

The latest update in the Waiting to Launch series, released today, continues to track the revenues, cashflow and capital expenditure of Canada’s biggest oilsands producers.

The Pathways Alliance, which represents Cenovus, CNRL, ConocoPhillips, Imperial, MEG Energy, and Suncor, maintains that its work to reach net-zero emissions by 2050 has not stopped, but that recent changes to federal greenwashing legislation preclude its ability to publicly disclose that work. However, Pembina Institute analysis of the companies’ financial results and statements to investors found no indication that capital is being allocated to decarbonization work at a level that would indicate any projects – including the Pathways ‘foundational’ carbon capture and storage project – have progressed beyond the early stages of the project development process.

This is despite the existence of a suite of incentives to support such investments. For example, the passage in June of the federal Carbon Capture Utilization and Storage Investment Tax Credit triggered final investment decision announcements from other companies on commercial-scale carbon capture projects.

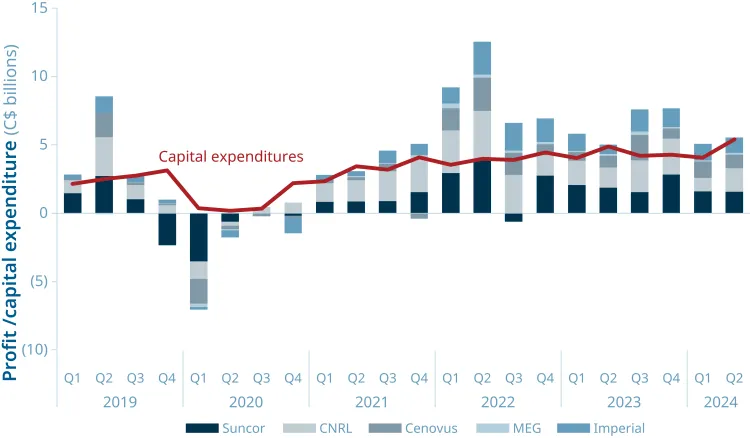

Meanwhile, Pembina Institute research shows that all six Pathways Alliance companies have instead allocated several billion dollars of capital to projects that will expand their production by tens of thousands of barrels per day over the next few years. This rush of activity is a further indicator of the continued strong financial position that these companies now find themselves in, building on two successive years of record profits. The opening of the Trans Mountain Expansion (TMX) pipeline in May has precipitated yet more favourable market conditions, which appears to have compelled companies to shift towards investing in growing production– but has notably not led to capital also being dedicated to decarbonization work.

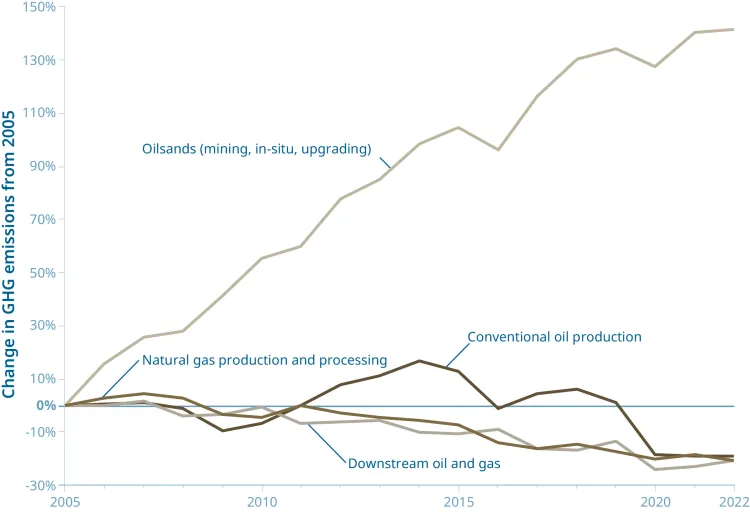

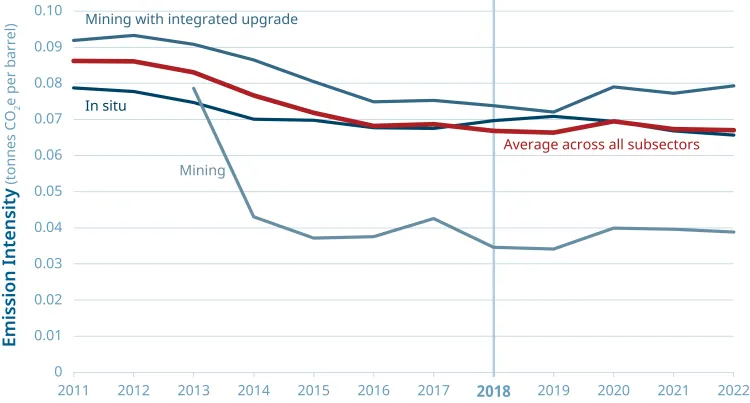

The report also finds that even modest gains in emissions intensity (the amount of carbon dioxide equivalent emitted per barrel produced), which the industry often cites as evidence of its environmental performance, have plateaued and begun to reverse – with average emissions intensity having in fact risen by 1% since 2018. In absolute terms, since 2005, emissions from Canada’s oilsands have grown by 142%, largely driven by increased oilsands production that has not been accompanied by substantive work on emissions. During the same period, emissions from every other oil and gas subsector (natural gas production and processing, conventional oil production, and downstream operations), as well as from other heavy industries, such as electricity production, have fallen, underscoring the pressing need for coherent regulations on oilsands emissions.

Key graphs

Oilsands emissions have increased by 142% since 2005, while they have fallen in every other oil and gas subsector.

Modest gains in emissions intensity in the oilsands have stalled and started to reverse – rising by 1% since 2018.

Profits in the oilsands sector have remained strong so far in 2024 after two record years, with capital expenditure now also being allocated to new production, but not to meaningful decarbonization work.

Quotes

“In terms of emissions, Canada’s oilsands sector is an outlier. Despite many years of pledges from the industry on improvements to environmental performance, its emissions have continued to climb sharply, even as they have fallen in every other oil and gas subsector.

“As our analysis shows, the oilsands industry remains highly profitable. It has now enjoyed two back-to-back record-breaking years in terms of profits, with export opportunities likely to remain favourable due to the opening of TMX.

“These facts underscore the need for coherent regulation that works in tandem with existing incentives to ensure this sector does its fair share to reduce its emissions.”

— Matt Dreis, Senior Analyst at the Pembina Institute’s oil and gas program

[30]

Contact

Alex Burton

Communications Manager, Pembina Institute

825-994-2558

Background

Op-ed: Greenwashing legislation has resulted in less talk from Pathways about their emissions reduction plans

Media release: Strathcona carbon capture partnership announcement positive step towards oilsands decarbonization

Report: Survival of the Cleanest: Assessing the cost and carbon competitiveness of Canada’s oil